Retirement Plans for Dentists

By Cecil Staton, CFP®

Retirement Plans for Dentists

Are you a dentist considering retirement planning? Arch Financial Planning is here to help. We offer financial planning for dentists and build retirement plans for dentists nationwide. Your dental practice and hard work are the foundation of your livelihood, so it's important to understand what options are best for your retirement plan. With the right plan, you'll have greater stability and security as you enter into a new stage of life. To get started, let's explore the retirement options available specifically tailored to dentists, such as 401(k) plans with profit sharing. Let’s get prepared today!

What Types of Retirement Accounts Exist for Dentists?

An Overview of Retirement Plans for Dentists such as 401(k) plan, SIMPLE IRA Plan, SEP IRA, and Cash Balance Plans

As a dentist, planning for your retirement savings is crucial for ensuring a comfortable life after retiring from your practice. Luckily, there are a variety of retirement plans available for dentists, such as the 401(k) plan, SIMPLE IRA, SEP IRA, and Cash Balance Plan. Each type of plan has its own unique benefits and requirements that should be carefully considered. To make the best decisions for your future, it's important to work with a financial advisor who can guide you through the options available to you, including exploring the possibility of also using a Roth IRA and taxable brokerage account. Whether you choose a cash balance plan or another type of retirement plan, taking the time to plan now can make a significant difference in your financial future.

What is a 401(k) Plan, and How Does It Work For Dentists

A 401(k) plan is a retirement savings plan that is offered by small-business owners, such as dentists. It is a type of plan that allows employees to save and invest a portion of their income for retirement benefits using tax-deferred or Roth options. What makes a 401(k) plan attractive is that it comes with employer contributions, which helps to boost retirement savings. For dental practice owners who are looking to provide their employees with a retirement savings plan, a 401(k) plan can be an excellent option. As long as they meet the eligibility requirements, any eligible employee can take advantage of this plan and start saving for retirement. With a 401(k) plan, dental professionals and their employees can enjoy the peace of mind that comes with knowing that their retirement is well taken care of.

Advantages of Setting Up a 401(k) Plan for Dentists

As a dentist, retirement planning is an essential consideration. Setting up a 401(k) plan can offer numerous advantages. For starters, it offers the ability to make safe harbor contributions to a qualified plan. Safe harbor contributions are essentially matching contributions that can help prevent plan participation issues. As the employer, you can make a non-elective contribution, which means you'll pay directly to your staff's retirement account regardless of whether employees make their own contributions. This helps you avoid the risks of discrimination testing against non-highly compensated employees, such as hygienists, dental assistants, and officer managers.

Another advantage is the potential to receive employee contributions, which can boost retirement savings even further. Compared to a traditional IRA, which only allows for annual contributions up to a certain limit, a 401(k) plan allows for much higher contribution limits which can significantly impact retirement savings. Ultimately, a 401(k) plan can help a dentist plan for a financially secure future, which is especially important in a profession where physical demands and long hours can make retirement seem very far away.

Since 401(k)s are tax-advantaged accounts, you won't pay capital gains if you sell or move money between funds within the 401(k) account. You don't pay tax until you've reached retirement age and withdraw the money from the plan.

Profit-Sharing Plans as an Option for Dentists

As a dentist, ensuring a secure financial future is incredibly important. A profit-sharing plan can be a great option for retirement savings. With this type of retirement plan, a percentage of the practice's profits are contributed to the plan, allowing dentists to save up for retirement while their practice continues to grow. Additionally, working with a tax advisor, such as Arch Financial Planning, can help navigate the complexities of setting up and managing a profit-sharing plan and may even lead to tax savings. By considering a profit-sharing plan as part of their financial strategy, dentists can take control of their retirement planning and feel confident in their financial future.

Ultimately, you'd contribute beyond your 401(k) Safe Harbor requirements with a profit-sharing provision. This allows even more tax deferral towards your own retirement.

Complimenting your 401(k) with a Cash Balance Defined Benefit Plan

If you're a plan sponsor that offers a 401(k), you may be aware of defined benefit plans and the contribution limits they come with. However, have you considered complimenting your 401(k) with a Cash Balance Defined Benefit Plan? Not only does this strategy offer additional retirement income, but it also provides tax benefits for both employers and employees. With a Cash Balance Defined Benefit Plan, employer contributions are tax-deductible, and the plan can be used to supplement the annual contribution limits of a 401(k). By combining the two plans, employees can enjoy the best of both worlds and set themselves up for a comfortable retirement.

Adding a Cash Balance plan is best for practice owners with income levels of $400,000 or much more. You must also have personal financial goals that allow you to contribute the maximum amount to qualified plans. Lastly, if you have non-owner doctors in the practice, the amount you have to contribute on their behalf could be prohibitive.

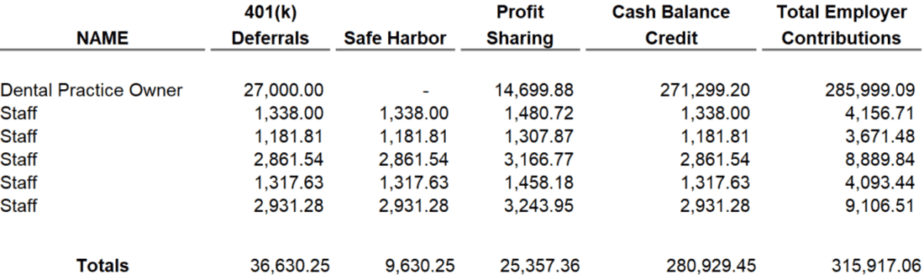

Examples of Cash Balance plan designs with 401(k) and Safe Harbor, and Profit Sharing Provisions

If you want to save much more money than the traditional 401(k) offers, consider combining a 401(k) plan with profit-sharing provisions and a Defined Benefit Plan. Cash balance pension plans are a defined benefit plan that may allow you as the owner of your dental practice, to contribute a significant amount towards your retirement.

The combination of these plans works well for dental practice owners with fewer employees and no associates. In many cases, you're the sole doctor in your practice or have an equal partnership with another doctor with very high collections and a desire to save significantly towards retirement.

The first example is a single doctor practice with numerous part-time employees who all work over 1,000 hours within each calendar year. A portion of their salary is paid into the plan either by their won deferrals or employer contributions (Safe Harbor, Profit Sharing, Cash Balance Credit). This doctor is nearing their retirement age of 60. Please note that this is for illustration purposes only. You will need to have an illustration done for your own circumstances.

As you can see, this doctor is able to contribute a considerable sum towards their retirement. The tax advantages of contributing more than 300,000 towards their retirement are massive. To recap, you're generally able to take a tax deduction for your employer contributions and your 401(k) deferral for your salary.

The Benefits of Starting Early With Retirement Planning

Retirement planning may seem like a distant future for many, but starting early can provide numerous benefits when it comes to your plan design and financial security. By beginning your retirement planning early, you can take advantage of tax benefits that will help reduce your overall tax burden. In addition, with ample time on your side, you can seek out quality advisory services that can provide invaluable insights and expertise in navigating complex retirement planning decisions. Ultimately, starting your retirement planning journey early can pave the way for a comfortable and secure financial future.

Why SIMPLE IRA Plans & SEP IRA Plans Aren't Desirable

While SIMPLE IRA and SEP IRA plans may seem like straightforward choices, they may not be the most desirable options. Both plans can be limited in terms of contribution amounts and rules. With SIMPLE IRA plans, the contribution limits are often much lower than traditional 401(k) plans. With SEP IRA plans, only the employer is able to make contributions, which means less employee involvement. Additionally, both plans can count towards the pro-rata rule when considering making a back-door Roth IRA contribution. As a dental practice owner, it's important to do your research and consider all options before deciding on a retirement plan for your practice.

Some like to use self-directed SEP IRAs to buy real estate. This is generally not advisable for many reasons. Also, SEP IRAs only offer nonelective contributions. In other words, only you, as the practice owner, are allowed to make contributions.

Secure Act 2.0 401(k) Start-Up Credit

Currently, dental practice owners can receive a start-up credit for costs related to setting up retirement plans. You're eligible if you have 100 employees or less who received compensation of $5,000 or more. You also must not have offered a retirement plan within the last three tax years.

You'll also receive a tax credit if you enable an auto-enrollment feature once you're employees become eligible. This will eventually become a requirement in 2025, but for now, you'll receive a tax credit.

How Working with an Experienced Financial Adviser Can Help

If you want professional help, Arch Financial Planning helps many dental practice owners model their employer-sponsored retirement plans. To get started, we'll discuss your cash flow and savings goals, followed by obtaining a census from your payroll. The next step is for us to calculate your potential contribution limits for defined contribution plans and consider your retirement goals. We'll help you determine if these plans are even right for you.

If you like the plan design and want to move forward, we'll help draft a plan document and pick the service provider for your TPA & record keeper. Next, we'll review investment options, such as mutual funds, ETFs, and CDs, to determine what's appropriate for your plan.

Can My Attorney Advise Me On Dental Retirement Plans?

Your dental-focused attorney can advise on retirement plans, but they should stick to only offering legal advice. Selecting and implementing investment options isn't something they can advise on without being registered as an investment advisor. Cash balance plans, in particular, are best left to someone who is allowed to give investment advice and has extensive experience using them.

Conclusion

If you're in the dental industry, you may have a lot on your plate when it comes to financial planning. Between a traditional retirement plan, student loan debt, and varying income levels, it can be tough to navigate. That's where an experienced financial adviser comes in. They can guide you through the process, helping you create a personalized plan that takes into account all of your unique financial needs and goals. With their expertise, you can feel confident that you're making the best decisions for your financial future. So why navigate these waters alone? Reach out to a financial adviser and take the first step toward a brighter financial future.

Retirement planning for dentists may seem daunting at first. But by familiarizing yourself with options like a 401(k) plan, SIMPLE IRA, SEP IRA, and Cash Balance Plan, as discussed in this article, you can start to make sense of it all and choose the savings plan that works best for you and your goals. Furthermore, don’t forget to consider the advantages of adding a profit-sharing plan as well as a cash balance defined benefit plan. Also, keep in mind the importance of considering retirement early on. As Arch Financial Planning has extensive experience in providing dental professionals with sound financial advice and strategies—it is worth consulting with an experienced professional to get started off on the right foot. There are certainly enough viable options available for most any budget—in order to create a solid retirement plan. When you're ready to begin planning or answer any questions you have about taxes or fiduciary services required of employer sponsored plans—Schedule an introductory call today!

Related Reading: Physician Mortgage Loans | Arch Financial Planning

Related Reading: Tax Planning for Doctors | Arch Financial Planning

Related Reading: Financial Planning for Early Career Doctors - Arch Financial Planning

Related Reading: Estate Planning for Doctors - Arch Financial Planning

Author: Cecil Staton, CFP®

I'm a fee-only financial advisor serving clients locally in Athens, GA, and virtually nationwide.

I left the large financial institutions to start my own firm so people could pay for real planning, not just a hidden agenda to sell a product.

As a fiduciary, Arch Financial Planning, LLC was built on that promise by delivering non-cookie-cutter plans that provide solutions to achieve their goals and act in their best interest.

Who do I serve?

Typical: Retirees & High-income households

Goals: Lower taxes, optimize investments, retire early & confidently

Location: Virtually anywhere in the U.S. and locally in Athens, GA

Want To Be Smarter With Money Than Your Friends?

Want to make smarter financial moves than your peers? Our exclusive newsletter delivers insider insights, expert strategies, and the 7 BIGGEST steps to maximize wealth, minimize taxes, and achieve financial freedom.

Topics Covered:

🔹 Reduce Your Tax Burden with Smart Planning

🔹 Retire Early & Secure Financial Independence

🔹 Build a Diversified Investment Strategy

📩 Join thousands of high-income professionals leveling up their financial game. Sign up now and get our latest comprehensive guide—FREE! PS: We hate spam and will NEVER sell your email. Unsubscribe at any time.

Disclaimer:

This website (the “Blog”) is published and provided for informational and entertainment purposes only. The information in the Blog constitutes the Content Creator’s own opinions and it should not be regarded as a description of services provided by Arch Financial Planning, LLC or Cecil Staton, CFP® CSLP®.

The opinions expressed in the Blog are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. It is only intended to provide education about personal financial planning. The views reflected in the commentary are subject to change at any time without notice.

Nothing on this Blog constitutes investment advice, performance data, or any recommendation that any security, portfolio of securities, investment product, transaction, or investment strategy is suitable for any specific person. From reading this Blog we cannot assess anything about your personal circumstances, your finances, or your goals and objectives, all of which are unique to you, so any opinions or information contained on this Blog are just that – an opinion or information. You should not use this Blog to make financial, tax, or legal decisions, and we highly recommend you seek professional advice from someone who is authorized to provide tax, legal, or investment advice.