Economic & Market Outlook Through June 2022

Economic Headlines Impacting Markets Through June of 2022

On the positive side, the economic impact of COVID-19 has continued to fade through 2022 as case counts in the United States have lowered and travel restrictions are easing relative to the start of the year.

Conversely, I don't expect the federal government to further any significant fiscal stimulus through the end of 2022 and into 2023. Therefore, consumer spending on essential goods and services should grow slower through the rest of the year and into 2023.

The Russian invasion of Ukraine has caused disruption far beyond the Ukrainian border. Sanctions in Russia have caused an increase in commodities such as food and energy prices. I am hopeful that there will not be a further escalation, and the producers of commodities will adapt by promoting more supply.

Inflation

Inflation has soared over the past six months due to increased demand and supply chain disruption. Countries abroad, such as China, continue to hold a "zero-Covid" policy. Fatalities should be lower, but the lockdowns will disrupt exports and global supply chains.

Mortgage rates have quickly increased due to the Federal Reserve's high inflation and interest rate hikes. While mortgage rates have spiked rapidly, it's important to remember that they're still historically low.

Economic momentum has many headwinds, including further rate increases, fiscal drag, stock market losses, and record-low consumer sentiment.

US Stocks

US stocks have had their worst first half since 1970, with the S&P 500 down 21%. While that doesn't feel good for anybody, this isn't the end of the road for long-term investors.

However, there are plenty of bright spots for long-term investors that follow our strategy. Arch Financial Planning, LLC tailors portfolios to capture market returns but tilts toward small, value, and profitability factors.

We believe that stock valuations in the US have dropped to more reasonable levels based on long-term relative valuations. Traditional valuation metrics support this within most asset classes and sectors of US stocks.

Value Remains Attractive Relative to Growth

Value stocks are still relatively cheap compared to growth and tech stocks, even considering the massive sell-off of tech stocks in the first half of 2022.

Small-cap value stocks, in particular, continue to hold attractive valuations relative to large-cap growth stocks. These facts present great opportunities for long-term and disciplined investors.

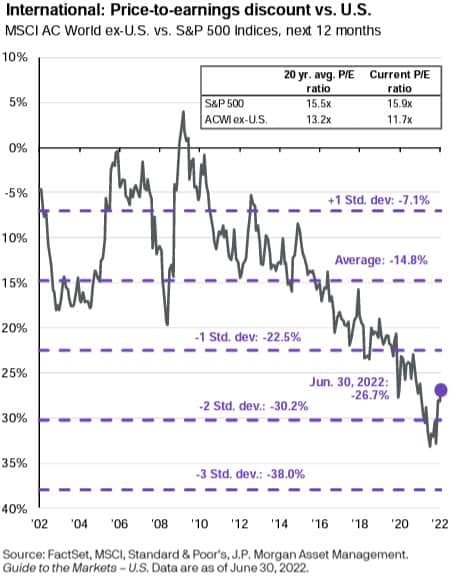

International Stocks

International stocks continue to hold an attractive relative valuation compared to US stocks. Currently, I do believe that US stocks deserve a premium over international stocks. However, the spread of that premium makes international stocks attractive relative to large-cap US stocks.

China's zero COVID-19 policy continues to drag emerging markets stocks. While this policy will lower case counts and fatalities, it will also slow global economic growth and the growth of the emerging market asset class.

We are still in the most extended cycle of outperformance of US stocks relative to international stocks that I've tracked since the early 1970s. When will the nearly 15-year period of outperformance end? In the past, these cycles have rotated between international and US outperformance with more regularity, never more than 7.5 years.

I am not in the business of predicting when international stocks will outperform US stocks again. However, I continue to preach the importance of diversification and sticking to your investment strategy.

Bonds

For most of the last 30 years, interest rates have decreased. As a result, the price of currently issued bonds increased. Conversely, in 2022, we've seen a sharp increase in interest rates, hurting bond investors.

Our bond portfolios have held short-duration Treasury bonds due to the low-interest-rate environment and diversification benefits. Treasury bonds tend to be more uncorrelated to stocks relative to other bonds.

I expect more bond headwinds as the Federal Reserve projects more interest rate increases. However, intermediate-term Treasury bonds and shorter-duration corporate bonds are looking more attractive.

Credit spreads (difference in rates between corporate rates and Treasury rates) are widening due to weakening economic expectations. With current credit spreads, exposure to credit risks such as lower-quality corporate bonds and convertibles may have value. Of course, this assumes we can avoid a deep economic downturn.

Conclusion

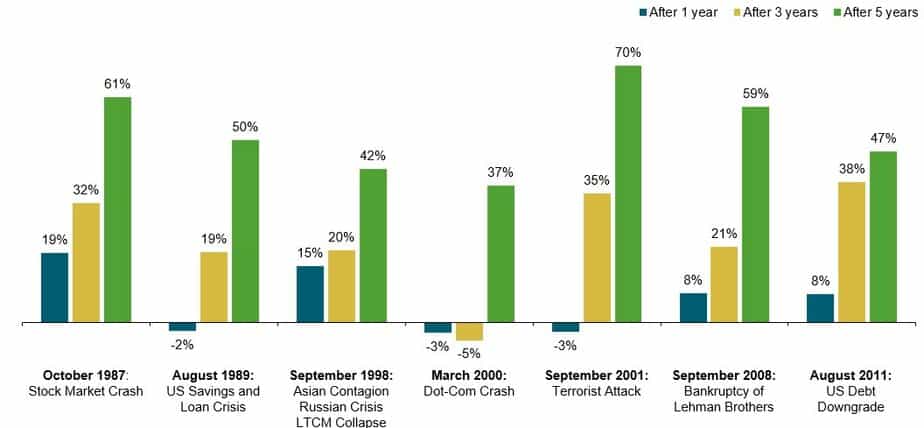

Can you imagine if the financial news media would preach responsible, long-term, buy-and-hold investing? While that would make for a dry news cycle, it has worked well for long-term investors. After every market downturn in history, strong market returns have followed.

It's critically important to remember that market declines are expected and will happen numerous times throughout your time as an investor. In the short run, we will see returns all over the place. However, you'll experience positive performance more likely than not when you look at more extended periods.

Higher interest rates in the US and other economic headwinds make a strong case for diversification beyond just the S&P 500. However, the evidence shows that tilting your portfolio towards small value and diversifying into international remain attractive. We remind our clients that they will be rewarded by sticking to their diversified investment strategy over long periods.

If you're still curious, you can subscribe to our newsletter and learn more about our services at:

Disclaimer:

This website (the “Blog”) is published and provided for informational and entertainment purposes only. The information in the Blog constitutes the Content Creator’s own opinions and it should not be regarded as a description of services provided by Arch Financial Planning, LLC or Cecil Staton, CFP® CSLP®.

The opinions expressed in the Blog are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. It is only intended to provide education about personal financial planning. The views reflected in the commentary are subject to change at any time without notice.

Nothing on this Blog constitutes investment advice, performance data, or any recommendation that any security, portfolio of securities, investment product, transaction, or investment strategy is suitable for any specific person. From reading this Blog we cannot assess anything about your personal circumstances, your finances, or your goals and objectives, all of which are unique to you, so any opinions or information contained on this Blog are just that – an opinion or information. You should not use this Blog to make financial decisions and we highly recommended you seek professional advice from someone who is authorized to provide investment advice.